Microeconomics Definition

Microeconomics is a branch of economics that studies the allocation of scarce resource among alternative purposes. It analyses the behavior of individual agents; as opposed to macroeconomics, that studies the behavior of economic aggregates. Microeconomics focuses on individuals, families and companies.

One of the main purposes of microeconomics is to analyze the mechanisms that establish the relative price of goods and factors and to study the effects that different institutions have on key variables such as market price, quantities traded and benefits for the companies and utility for consumers. The institutions analyzed by microeconomics can be different market structures (perfect competition, monopoly, oligopoly, etc.), the effects of varying types of taxes, etc.

Microeconomics uses formal models to explain the behavior of producers and consumers. Microeconomics models use assumptions to arrive to conclusions using a deductive method. The analytical method of microeconomics is based on logical reasoning. Mathematical language helps to clearly express the reasoning and increases the stringency level. This is why microeconomics tends to use mathematical language.

During the last decades, microeconomics has narrowed its ties with macroeconomics. Modern aggregate models include microeconomic fundamentals which allow for more solidity in formal terms. For example, the aggregate consumption function (which explains the behavior of many individuals) in macroeconomic models, must be consistent with the microeconomic behavior function (which explains the behavior of a single individual).

Microeconomic Examples

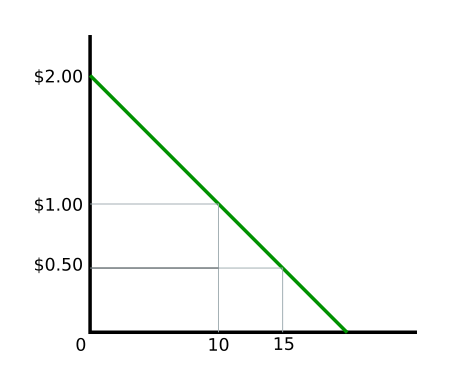

Example 1: Demand

If the price of a pencil is $1, John will be willing to buy 10 pencils. If the price is $0.5, he will be willing to buy 15. But if the price increases to $2, he wont buy any pencil at all.

Estimate the individual demand for John, assuming a linear demand function:

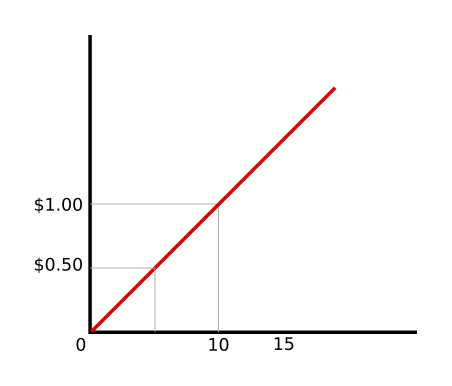

Example 2: Supply

If the price of a pencil is $0.50, Mary will be willing to sell 5 pencils. If the price increases to $10.00, she will be willing to sell 10 pencils.

Estimate the individual supply curve for Mary, assuming a linear supply function:

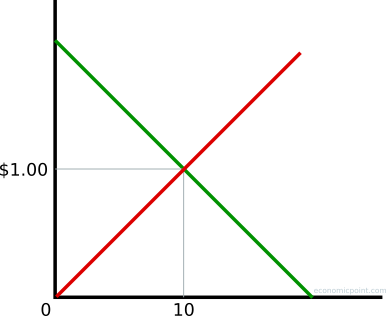

Example 3: Supply and Demand

If Mary and John are the only participants in this market, what quantity of pencils will be traded and at what price?